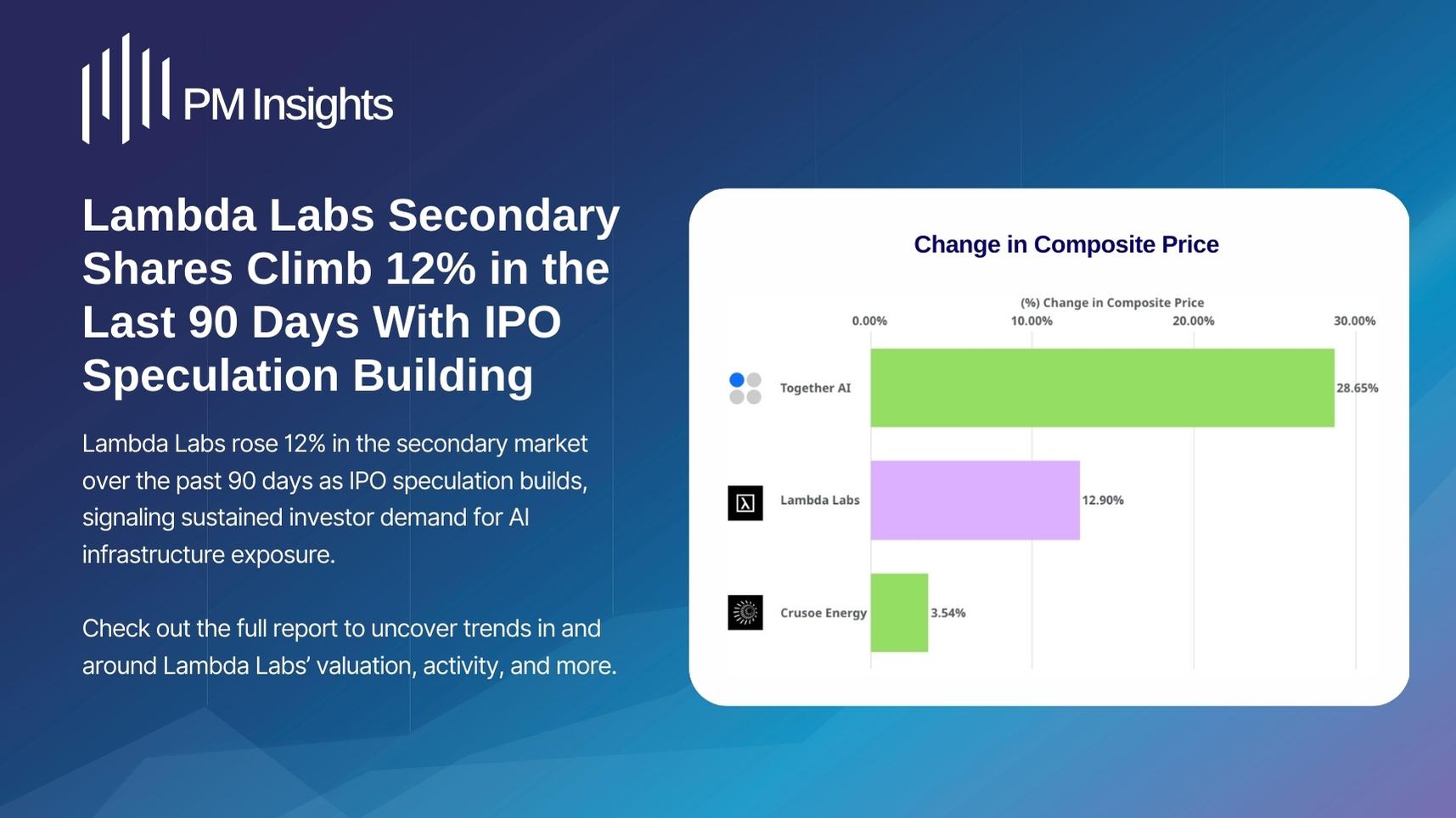

.jpg)

Mixed Results for Mutual Funds' Private Equity Mark to Market

Mutual funds continue with lowered valuations on private stocks

December 6, 2022

The Case for Mark to Market:

Funds holding private assets finally realize that business as usual is no longer good enough. The ability to mark to to the last round's price (or par acquisition) is virtually irrelevant given the current dynamics in the private market.

Some managers continue to ignore the private market’s equity fallout YTD of -34.19% through November, as tracked by the ApeVue50 index of the 50 most active unicorns in the secondary market. Notably, some index component issuers are down significantly more than the index itself, such as Klarna (-82.91%), Stripe (-62.97%) and Databricks (-50.46%). Across these three aforementioned stocks, Klarna has taken a very public down-round, Stripe has reportedly slashed its internal valuation, and Databricks' stock has been marked down due to varying factors.

Most managers with whom ApeVue has spoken are either already remarking, or are in the process of evaluating their valuations coming into year end.

Mutual Fund Marks v Daily Market-based Databricks Pricing:

Taking a closer look into Databricks, which has recently signaled growing staff in San Francisco by acquiring further office space while their peers downsize, illustrates the spectrum of valuation in the market. While Databricks has declined 50.46% ytd, it posted a modest gain in November, outperforming the ApeVue50 index decline of ~4.5% last month.

Dissecting the SEC reported pricing from BlackRock, T. Rowe Price, and Fidelity this year, the three funds marked their Databricks positions down as early as Q1. Data suggests T. Rowe Price’s New Horizons Fund reduced the value of its holding around 25% at the end of March. SEC data sourced by ApeVue concludes that the Fidelity Puritan Trust likely held their position values static until they revised their level down by ~25% around mid year. In contrast, BlackRock’s Global Allocation Fund was first to deviate from the “last round” price, with reports showing their 2021 year end closing valuation was ~8% below the last round pricing which had valued Databricks at $38-billion.

Interestingly, the most recent level seen from BlackRock for the fund (September 30th, 2022) implied Databricks' valuation of ~$31.6-billion. Fidelity’s and T. Rowe Price’s for the same date implied a valuation of $28.3-billion, over 10% variance from BlackRock. ApeVue’s implied valuation for September 30 was also around $28 billion, but the ApeVue valuation at November 30 had fallen to $26.4-billion, or just over 30% below the valuation at the long outdated August 31st, 2021 funding round.

(Note: Inferred implied values account for a recent 1-to-3 stock split, but lack knowledge of exact share changes following the prior round, and at a minimum lack dilution related changes.)

Private Matters:

Where are pensions, endowments, and other funds marking Databricks and other holdings battered by 2022's downturn? How many have left valuations static since a portfolio company’s last funding more than a year ago? For most, it will be hard to refute a markdown to the likes of risk teams, LPs, auditors, and soon regulators, especially given the actions taken by other fund managers. As we reach the end of 2022, one of the most important advances for the funds industry is the advent of independent, composite pricing of private company stocks through ApeVue. We believe our data are useful tools for fund managers and also predictors of how aggressive daily/monthly NAVs will change, along with where future rounds or M&A activity will invariably result.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

Ready to see it in action?

Schedule a demo with one of our experts