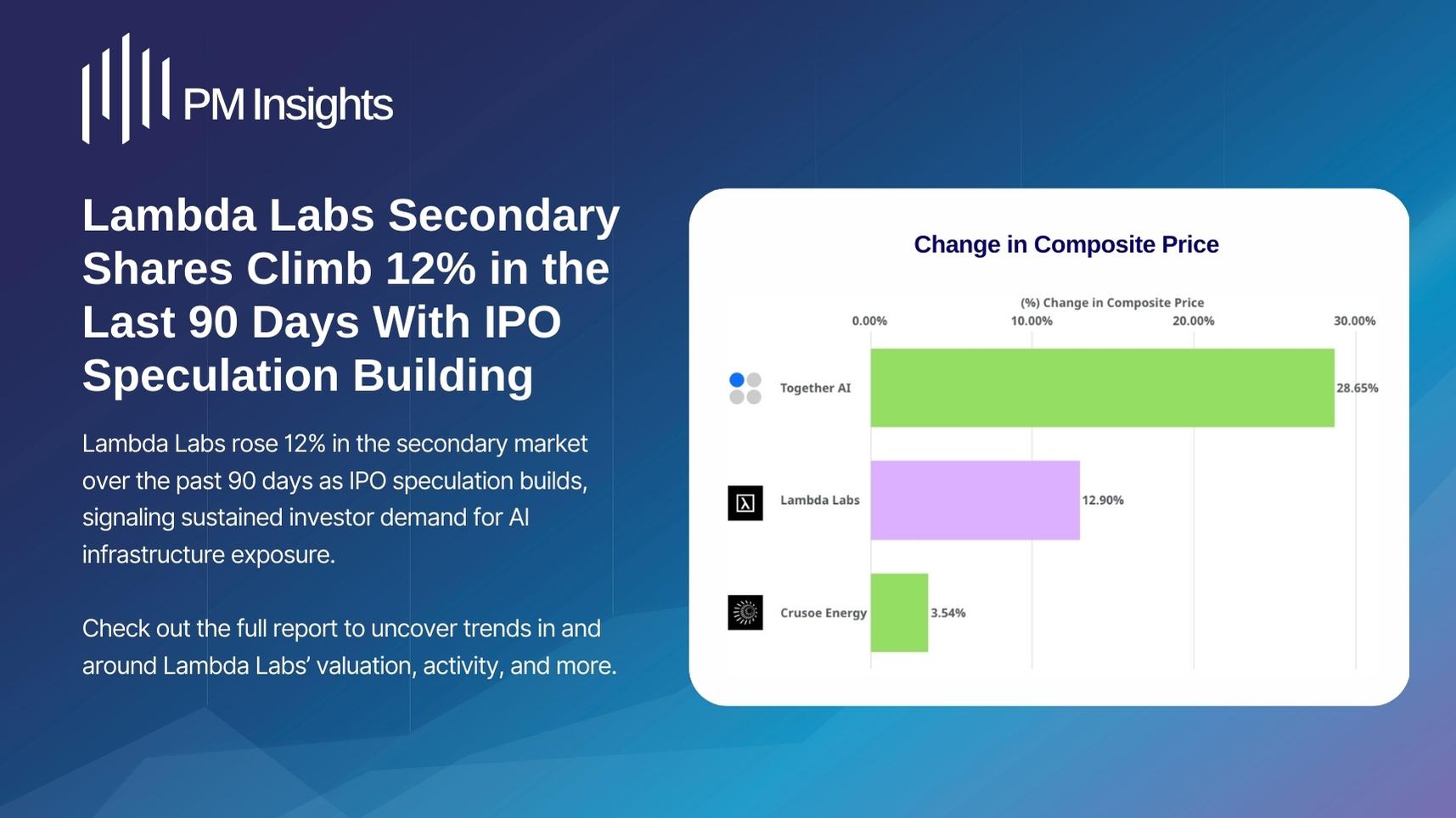

.jpg)

PM Insights 2024 VC Market Review

Market data insights for venture-backed private companies.

January 1, 2025

PM Insights 2024 Reflection

by Founder & CEO at PM Insights, Nicholas Fusco

My prediction a year ago was, "Private markets are going to be more relevant than ever in 2024." Given that our PM Insights pricing platform sits on hundreds of thousands of data points in the private markets, I already saw a rebound forming, but it was more profound than pure performance metrics.

In the past 12 months, seismic AI advancements originated predominantly from private companies versus public peers, and many public companies increased investment in pioneering private companies, and with continued IPO abstinence, this prediction proved accurate and will carry forward.

2025 brings a new (or re-newed) administration to Washington, eager to shakeup policies from the last 4 years. Investors will be better served by aligning with what remains consistent amidst change rather than predicting the next big shift.

Overweighting private stocks has historically maintained competitive advantages, which should persist through turbulence, offering benefits from lower taxes and potential exemptions for America's Great Wealth Transfer.

A less aggressive regulatory governance benefits private stockholders through fewer M&A restrictions and less scrutiny on complex transactions. PM Insights supports this landscape with vital valuation data and analysis.

As pioneers of the first daily, independent private stock pricing mechanism, PM Insights continues growing its client base and capabilities rapidly. Our transparency promotes sophisticated investor access, and we look forward to tracking the best private companies with you this year.

PM50 Growth Index YoY ROI

PM50 Growth Index ‘21 ‘22 ‘23 ‘24

.png)

Long Live 2021 ROIs.

Though the days of sky-high valuations that blessed late-stage private share sellers in 2021 are over, 2024 was the year of the sustained rebound in private company valuations.

Top-tier private companies, like SpaceX, Databricks, Revolut and Stripe were among those that took advantage of the resurgence in their valuations by running secondary market offerings, unlocking liquidity for their investors, employees and raising some capital to boot.

Expect more of the same in 2025, across a broader range of companies, along with more successful IPOs to build on the successes of the few like Rubrik & ServiceTitan that began to re-open the door in 2024.

Private & Public Market ROI

YTD ROI Selected Private Sectors

.png)

YTD ROI Private vs Public sectors

.png)

Sector ROI Change ’23 to '24

.png)

Most sectors see ROIs improving vs ‘23

The Financial sector (including Banking, Payments, and Investment tech) had a strong year in 2024. This success was driven largely by Revolut's fundraise at a premium valuation, along with Stripe and Klarna's significant recovery from their losses over the previous two years. Their resurgence helped lift valuations for a number of their smaller competitors as well.

Also, AI and related companies in Data, Automation & Infrastructure had a strong showing driven by the continued hype around AI and AI-adjacent companies.

Observed Activity Split by Structure Type

<row>

<col>

Direct vs SPV as % of Volume

.png)

</col>

<col>

Direct vs SPV as % of Count

.png)

</col>

</row>

SPVs continue to grow their share of secondary market activity

The share of SPVs as a % of overall market activity rose in 2024, with both % share of volume and total observed trades & IOIs growing YoY. The fact that volume % increased substantially more than total count % indicates SPVs are increasingly used in larger, institutional sized transactions rather than smaller retail deals.

This trend signifies growing appetite for secondary market liquidity among existing institutional players (some previously expecting it from now-scarce IPOs), as well as new market entrants both at institutional level and an increasingly active RIA community looking to unlock access to this tech-heavy market segment for individual investors, who historically would have waited until IPOs for access.

Given growing interest and increasing company willingness to engage with the secondary market, these trends will likely continue through 2025, further fueling growth in the cottage industry around SPV set-up and servicing.

Private Companies ROI During 2024

Percentage of Companies with a Positive/Negative/Flat ROI 2024

.png)

Mainly up and to the right.

Returns across private companies largely mirrored PM50 Growth benchmark's positive trajectory, with only 3 months showing net negative returns in 2024. Market confidence strengthened as industry leaders like SpaceX, OpenAI, Anthropic, Revolut, Stripe, and Databricks secured funding through primary raises and secondary markets – some multiple times – at increasingly higher valuations.

While H2 2024 benefited from easing monetary policy, 2025's outlook remains robust even without anticipated rate cuts. Investors are actively (re)entering the market, drawn to AI innovation and its infrastructure, alongside surging Aerospace and Defence sectors. The latter's growth is driven by governments increasing defense capabilities amid an increasingly volatile global environment, paired with accelerating space exploration initiatives.

Revenue Multiples for a few of the Most Active Companies

.png)

Note: The brief spikes in the data are due to new funding rounds / tenders that occurred

Revenue multiples for the most active companies on the rise.

Given the rising valuations in 2024, its no surprise that the revenue multiples have been rising in tandem.

The most notable growth has been from SpaceX, as they almost doubled their valuation in 2024, so their revenue multiple climbed most steeply, esp. towards year end, on the back of the blockbuster $350B valuation set for their latest tender offer.

Anthropic was not far behind also raising multiple times in 2024 at ever higher valuations, thus driving up the multiple.

Stripe was the notable exception, expected to grow their revenue at almost the same pace as their valuation in 2024.

Full Year 2024 Bid:Ask Spreads & Volatility of Composite Price

.png)

Both spreads and volatility ended the year higher than they started.

Despite overall lower volatility than 2023, spreads followed an interesting pattern – initially narrowing in late 2023 and early 2024 before widening throughout the year, though remaining below the extreme levels seen in 2022-23.

While top names enjoyed steadily improving liquidity through 2024, persistent pockets of illiquidity remained. These illiquid segments particularly affected smaller companies, where both positive and negative newsflow triggered sharp price movements, accounting for much of the market's volatility.

Sector Volatility & Bid:Ask Spreads 2024

<row>

<col>

Average Sector 90 Day volatility

</col>

<col>

Average Sector Spreads

</col>

</row>

Liquidity and hype driving spreads and volatility.

Higher spreads and volatility was seen across a number of sectors but for very different reasons:

Some sectors such as Privacy, Marketing and Logistics were suffering a lack of liquidity and hence were more volatile.

While others, like Neobanks, AI & DeFi were seeing more hype, increasing interest and resulting activity driving the volatilty (and returns) up.

The meteoric rise in interest towards some new entrants (such as xAI and Groq, among others) also contributed to volatility in 2024.

Average Bid & Ask Spread per Sector

.png)

Quarterly Bid & Ask volume

.png)

Bids regain momentum in the second half of the year.

Offers still make up the lions share of observed volume and after the spurt in bid-side share at the end of 2023 and in early 2024, Q2 again saw a tilt towards the sell-side once again.

This was in part spurred by some of the demand being satiated by some large secondary offerings coming directly form the companies and not through the brokers. It was short-lived however, with secondary market bid-side activity bouncing back to its trendline, on the way to recovering post the trough in late 2022 / early 2023.

Mean Volume per Indication Type

Quarterly Average Volume per Bid, Ask, & Trade

.png)

Average volumes remain compressed vs 2021 highs.

Overall, average volumes remain subdued across bids, offers and trades. Despite higher numbers of activity across the board, the averages are either unchanged or even lower than they were in 2023.

This is in line with reports of increasing numbers of new entrants in the space participating with smaller check-sizes, balancing out the increasing activity from larger institutions.

Top 10 by Volume

<row>

<col>

Top 10 Private Companies Based on Total Bid & Ask Volume

.png)

</col>

<col>

SpaceX and Bytedance remained dominant in 2024.

Volume based on observed broker activity has been dominated by the two titans - SpaceX & ByteDance, along with AI and large fintechs making up the remainder of the top 10 companies in 2024.

Having said that, Databricks had the largest funding round of 2024, with OpenAI, Anthropic and xAI also raising multiple billions through combinations of primary and company-led secondary sales, which are not reflected in this data.

</col>

</row>

Top 10 Based on Bid or Ask Volume in 2024

<row>

<col>

Bid Volume

.png)

Fintech, Aerospace & Defence and AI

SpaceX, Stripe & Anduril topped the observed bid-side secondary volume in 2024, indicating renewed interest in Aerospace & Defence. Predictably, AI names were in the mix, along with a number of other larger Fintech names. Also, ByteDance, though no longer at the top, remains one of the most liquid names since 2021.

</col>

<col>

Ask Volume

.png)

SpaceX & ByteDance

The two largest private companies continued to dominate sell-side activity in 2024. However, while SpaceX has seen a surge in both buy and sell-side activity, ByteDance sell-side activity has been much more pronounced in 2024.

</col>

</row>

Volatility of Top 10 Companies 2024

<row>

<col>

Change in Volatility ‘23 to '24 for Top 10 Private Companies*

</col>

<col>

Volatility in 2024 for Top 10 Private Companies*

</col>

</row>

.png)

(*) Based on Total Bid and Volume

Groq, the volatile.

AI was a volatile sector in 2023 as new entrants burst onto the scene and proceeded to quickly gain momentum and value. Some of these, Anthropic and OpenAI most notably, have since stabilized at the much higher valuations they now command. However, other new entrants, namely Groq, saw an uneven performance throughout 2024, in part due to hype and speculation that created a burst in valuation earlier in the year, which was later tempered by the realities of the company and the valuation at which it ended up pricing their round. Both SpaceX and Revolut had saw tremendous valuation growth, driving the volatility.

Top 10 Biggest Gainers & Losers for 2024

<row>

<col>

Top 10 Private Companies Based on Change in Price

.png)

</col>

<col>

Bottom 10 Private Companies Based on Change in Price

.png)

</col>

</row>

Revolut is riding high.

Revolut outshone all the AI companies on the back of strong results for 2023 and the approval of their banking license, allowing them to orchestrate a secondary sale at a bumper valuation. CoreWeave and Cerebras were not far behind, riding the AI infrastructure wave. Given their already hefty valuation, an almost doubling in value from SpaceX is also an incredible result.

Proportion of Change in Valuation

.png)

92% of companies in PM Insights’ universe were valued higher in their most recent round compared to previous round.

On the other hand, 43% of companies traded at had higher valuation compared to their most recent round, pointing to a ways to go to recovering some of the investments made in the heady days of 2021. Though progress is being made, as only 35% of companies had positive valutions since last round in Q3'24 .

PM Insights Price vs Mutual Fund Price

Pm Insights vs Mutual Fund Price Difference (quarterly Mean)

.png)

Historically, mutual funds have marked their positions in late-stage private companies at or above the most recent primary funding round valuation.

As market cooled off many of these funds were still slow to reflect the overall market sentiment, and increasingly PM Insights’ pricing (based on institutional secondary market activity) was below most mutual fund marks for those companies. However, this trend appears to be reversing per the numbers seen in Q2 & Q3 2024 (filings are a quarter delayed typically), which is in line with broader market recovery and positive dynamics, along with a growing number of funds marking more in line with the observable secondary market activity.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

Ready to see it in action?

Schedule a demo with one of our experts